Personal finance for normal people who like numbers. Real decisions, real tradeoffs, and the boring middle—without the hustle-culture fluff.

Get the Cash Buffer framework (free)

I’ll send you the simple framework + occasional new posts (about 1×/week). No spam.

Recent Posts

-

Why I keep about $150k in cash and I’m not sorry about it.

Read more: Why I keep about $150k in cash and I’m not sorry about it.In personal finance, cash gets dunked on. “Invest everything.” “Don’t let money sit.” I get it. Over the long run, cash usually loses to inflation and it almost always loses to equities. And still, I keep about $150,000 in cash. Not because I’m confused about “cash drag,” but because right now cash is buying me…

-

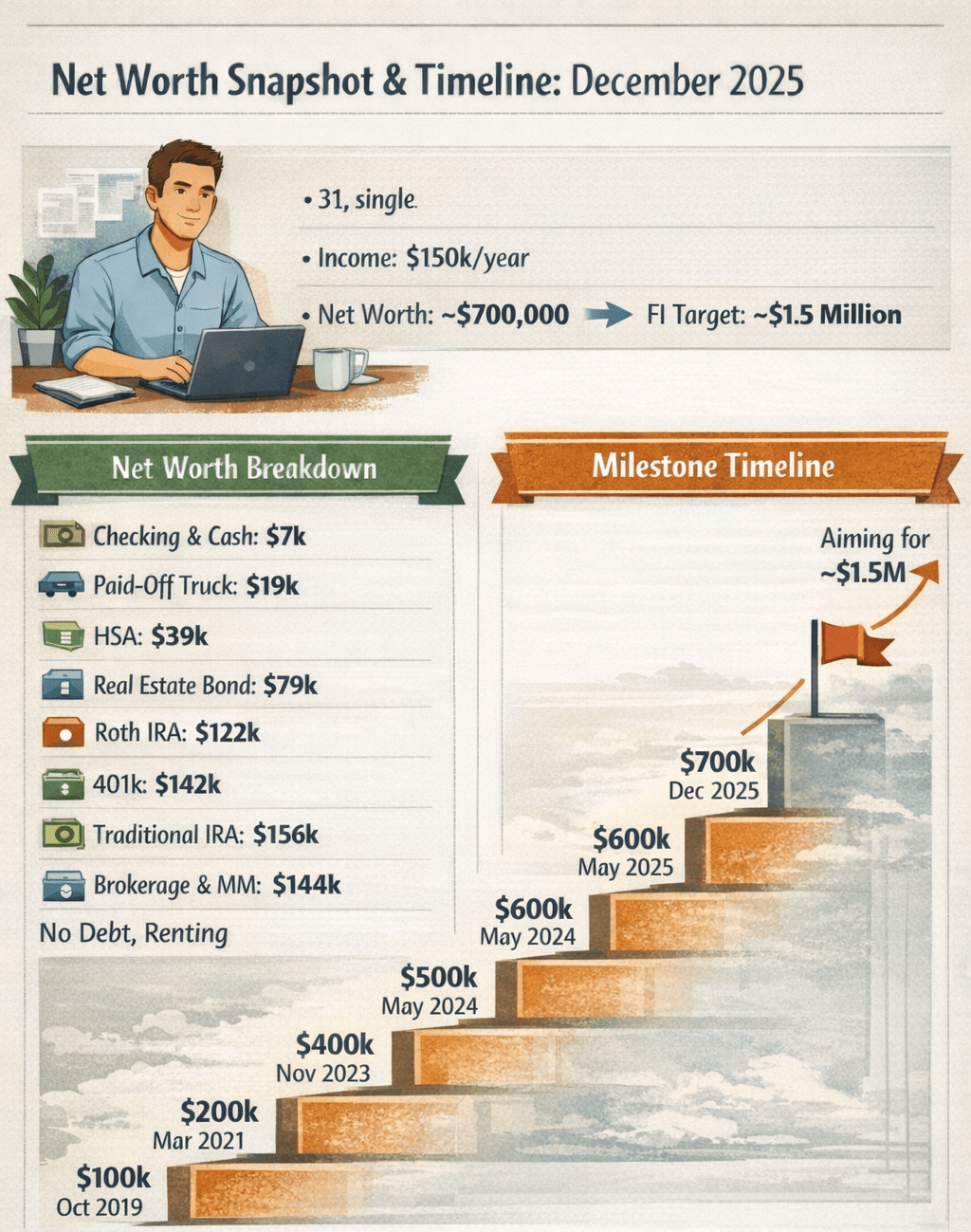

Breaking down my $700k net worth at age 31

Read more: Breaking down my $700k net worth at age 31A little bit of context up front. I’m 31, single, and I work in corporate strategy. Sharing real numbers can be genuinely helpful—especially when you’re not selling a course or pretending the path to financial independence is exciting every day. In December 2025, my net worth is about $700,000. I make roughly $150k per year,…